Last week the Securities and Exchange Commission (SEC) proposed sweeping changes to Regulation Crowdfunding (equity crowdfunding or Reg CF) as well as the other private capital-raising exemptions. The proposals come just months after the SEC closed comments on last summer’s Concept Release. The commission sought to harmonize, simplify, and streamline the exemptions. As SEC Chairman Jay Clayton stated, “The complexity of the current framework is confusing for many involved in the process, particularly for those smaller companies whose limited resources spent on navigating our overly complex rules are diverted from direct investments in the companies’ growth. These proposals are intended to create a more rational framework that better allows entrepreneurs to access capital while preserving and enhancing important investor protections.”

The proposed changes to Reg CF are particularly significant. Congress enacted this exemption as part of the JOBS Act of 2012 to open the private markets to retail investors. The idea was everyone could invest in hotshot startups but also local businesses that supported communities. It would also allow entrepreneurs traditionally excluded from the angel investor/venture capital circuit a better chance to thrive by democratizing capital raising. Signs showed Reg CF had started to fulfill its potential. According to Crowdfund Capital Advisors, which curates equity crowdfunding data, since 2016 successful Reg CF companies had pumped almost one billion dollars into local economies.

Still, complaints persisted. Many companies thought the $1.07 million raise limit too small. And rules restricted Accredited Investors to relatively tiny amounts despite no such constraints with Reg D. Moreover, regulations forbade issuers from discussing and gauging interest in their raise before spending money on legal and accounting services. Finally, retail investors meant messy cap tables that dismayed later investors.

SEC addressed long-standing equity crowdfunding complaints in proposal

Yesterday’s proposal

solves all these issues and sets the stage for a paradigm shift in U.S. capital

raising. Among the potential rule changes:

Raise the overall to limit to $5 million: While not as big as some had hoped, this new ceiling allows for larger institutional players to invest alongside retail investors.

Remove Accredited Investor limits: Successful equity crowdfunds usually have a mix accredited and nonaccredited investors. Accredited Investors send important signals to each other and the larger market. Removing Reg CF’s arbitrary limit increases the chance for successful raises. And it partially eliminates the need to “stack” Reg Ds on top of Reg CFs so Accredited Investors can fully participate.

Allow ‘testing the waters’ communications prior to the raise: The ability to gauge interest in a raise before having to spend money on professional services is critical. Also, equity crowdfunding companies tend to be newer and less experienced with complex securities laws. This gives companies a better idea of their raise metrics, while still protecting investors. by preserving liability for misleading statements.

Allow Special Purpose Vehicles: Allowing issuers to “clean up” their cap table by placing Reg CF issuers into an SPV was perhaps the most consistent Reg CF failing. According to the SEC proposal: “In particular, public feedback has indicated that allowing the use of such vehicles could address concerns associated with managing the potentially large number of direct investors that could result from a crowdfunding offering, as those investments would be held through a single purpose entity.” This also alleviates concerns about Reg CF issuers having to prematurely register as public companies.

Equity Crowdfunding can explode under proposal

Indeed, these long-sought changes could have lasting effects on the private capital markets. It could truly democratize capital raising, allowing everyone an equal opportunity at potentially lucrative investments. It could encourage entrepreneurs normally off the angel investor/venture capital radar to bypass traditional-funding methods. And issuers can synergize crowd effects by melding their investors, supporters, and customers. And it could geographically disperse capital investing away from the few hubs where it currently happens.

According

to the SEC press release, the comment period will remain open

for 60 days following the publication of these proposals in the Federal

Register.

The Telegram SEC fight over whether “Gram” tokens are securities progressed when Telegram ‘answered’ in federal court. The move foretells a lengthy battle, something Telegram surely hoped to avoid. Telegram’s Answer spotlights myriad government crypto failures. Among them, mixed signals by officials, selective enforcement, policymaking by staff, unclear rules, and bureaucrats protecting agency power. Regardless of the SEC Telegram outcome, without changes America’s tech advantage will shrink whilst sinecures rise.

Telegram’s two defenses against SEC enforcement

Telegram has two defenses but only uses one lest they admit

clandestine attempts to skirt rules. Officially Telegram complains SEC rules

are vague, scattershot, and violate due process. “Plaintiff has engaged in

improper ‘regulation by enforcement’ in this nascent area of the law, failed to

provide clear guidance and fair notice of its views as to what conduct

constitutes a violation of the federal securities laws, and has now adopted an ad

hoc legal position that is contrary to judicial precedent and the publicly

expressed views of its own high-ranking officials.”

Yes. Telegram’s Answer

covers many ad hoc apparatchik games. The three horseman of reaction, Shallow-End

Jay Clayton, Bill the Butcher Hinman, and NPC

Valerie Szczepanik play hot potato whilst Crypto

Mom Hester Peirce stares incensed. Risk-averseness, so common to our three

million “public servants,” isn’t bad with nuclear policy, global warming, or

Ukraine favors. But here, their actions matter. The future American economy and

our place as world’s chief innovator is at stake. Whether a court accepts SEC

buck passing given DAO

and NPC

Valerie’s Dreadful Guidance is unclear. But the government has good odds.

The digital asset itself is simply code. But the way it is sold [determines whether it is a security.] But this also points the way to when a digital asset transaction may no longer represent a security offering. If the network on which the token or coin is to function is sufficiently decentralized—where purchasers would no longer reasonably expect a person or group to carry out essential managerial or entrepreneurial efforts—the assets may not represent an investment contract. Moreover, when the efforts of the third party are no longer a key factor for determining the enterprise’s success, material information asymmetries recede” and “the ability to identify an issuer or promoter to make the requisite disclosures becomes difficult, and less meaningful.”

Crypto startups see decentralization as the only way around SEC compliance

Lawyers have earned millions working Bill the Butcher’s

statement into the current capital framework. Most use Reg

D for SAFTs but whether this covers the actual tokens is unclear.

Blockstack

is the only successful Reg A+ offer thus far. In its offering

circular it stated it expects to be decentralized and leave securities

compliance within a year. Kik

took a different route. It claimed its “Kin” tokens were already

decentralized. And thus, like Bitcoin or Ethereum could avoid SEC

oversight.

Telegram chose the Kik route, arguing the potentially

disbursed 220 billion Grams would be de facto decentralized, but the SEC

stopped it. As one CoinDesk

commentator stated: “Last year, messaging platform Telegram funded the

construction of its TON blockchain with a private placement which guaranteed

future allocation of Gram tokens, which of course would be decentralized

enough to not need to go through a securities registration. The SEC was not

convinced.”

SEC filed against Telegram before it could claim decentralization

And the SEC laid bare Telegram’s plan in its temporary restraining order: “Indeed, by definition, the TON Blockchain can only become truly decentralized (as contemplated and promoted in the Offering Documents) if Grams holders other than the original Grams purchasers actually stake Grams… Stated differently, if the original Grams purchasers alone all immediately staked their holdings, the TON Blockchain would be centralized rather than decentralized and, therefore, subject to misuse and majority attacks.” [original emphasis].

Thus, both sides skate decentralization.

Telegram demurs because it would tacitly admit it tried to skirt SEC mandates.

The SEC avoids it because it’s somewhat unofficial.

Telegram SEC fight shows problems with government crypto policy

But whatever happens, the government’s inability to explain its policy is a fiasco.

Relying on outdated precedent: SEC Enforcement defines securities from the 1946 Howey case. That worked for orange groves, but the world has changed slightly since mid-20th Century. Judicial precedent restrains the SEC, but also empowers it. The SEC likes Howey because it yields broad discretion.

Guidance that confuses more than clarifies: Crypto entrepreneurs have clamored for clear rules beyond outdated cases. The SEC responded with NPC Valerie’s Dreadful Guidance. It took 6-months to complete. And likely cost taxpayers upwards of a quarter-million dollars. And it only worsened things adding more factors to the Howey Test, without any inkling of weight or even if that was all. Anyone outside “public service” would have been fired for such waste.

Insistence entrepreneurs get permission: Not only does the SEC not give clear rules but it insists entrepreneurs ask permission through lengthy negotiations or laborious no-action letters. These letters may take years or not come at all. And others can’t use them as precedent. It also favors insiders, those represented by major law firms or with staff relationships.

Bureaucrats make policy without responsibility: Every document, speech, or murmur by an SEC functionary comes with disclaimers. No one takes responsibility or accountability. Bill the Butcher has a doctrine named for him—heady stuff—but ask if his statements represent the SEC. NPC Valerie travels the country on taxpayer dimes, receives VIP treatment at conferences. Ask her to opine beyond NPC fashion ‘Howey, Howey, Howey.’

Real guidance comes through enforcement: The SEC can bankrupt a startup. It has no shareholders, no timelines, no need for profit, subpoena power, and essentially an unlimited budget. Try and cross them. They dare you.

SEC functionaries have hijacked crypto regulation

NPC

Valerie summed the government’s crypto stance in a short yet revealing

comment. “The lack of bright-line rules allows regulators to be more flexible.”

This is true but has other effects. It leaves regulators with massive discretion. This gives them enormous power over the economy with no responsibility for the results. It mandates entrepreneurs approach them hat-in-hand for permission. And it makes them sought after speakers on the conference circuit.

But it’s a zero-sum game. Every unit of power Ms. Szczepanik reserves for herself and her colleagues removes it from job producers. Indeed, every ambiguous pronouncement shunts billable hours to lawyers and compliance professionals instead of research or marketing. Those building tomorrow’s economy need the flexibility not bureaucrats. They will power our future long after Ms. Szczepanik takes her professorship or retires to a nonprofit.

Too few call out dreadful SEC crypto policy

A few, but only that, recognize the absurdity. Most

prominently is Commissioner Hester Peirce, aka Crypto

Mom. As a lone voice, she has repeatedly warned about this path:

The SEC staff recently issued a framework to assist issuers with conducting a Howey analysis of potential token offerings. The document is a thorough 14 pages. It points to features of an offering and actions by an issuer that could signal that the offering is likely a securities offering. If this framework helps issuers understand what the different Howey Factors might look like in an ICO context, it may be valuable. I am concerned, however, that it could raise more questions and concerns than it answers.

While Howey has four factors to consider, the framework lists 38 separate considerations, many of which include several sub-points. A seasoned securities lawyer might be able to infer which of these considerations will likely be controlling and might therefore be able to provide the appropriate weight to each. Whether the framework gives anything new to the seasoned securities lawyer used to operating in the facts and circumstances world of Howey is an open question. I worry that non-lawyers and lawyers not steeped in securities law and its attendant lore will not know what to make of the guidance.

Pages worth of factors, many of which seemingly apply to all decentralized networks, might contribute to the feeling that navigating the securities laws in this area is perilous business . . .

Congress could act to reign in SEC intransigence

Representative Warren Davidson (R-OH) stated:

Regulation by enforcement [has] all the charm and inefficiency of third-world power structures.

. . .

The SEC is doing a complete patchwork of regulation. No one knows where they’re going. They’re literally told if you want to launch a token, whatever you think you want to do with it, come check with the SEC first. . .. And you can grovel. If you grovel well enough, then we’ll give you a no-action letter. You have hundreds of companies waiting on no-action letters. They’ve approved two.

You can’t raise capital while you’re waiting for that.

Budd: In April Fin Hub published a framework for investment contract analysis of digital assets which included 60 plus factors for determining whether or not the SEC would consider a digital asset a security. In a statement released alongside your framework your colleagues Bill Hinman and Valerie Szczepanik indicated that the framework is not intended to be an exhaustive overview of the law. But rather an analytical tool to help market participants . . . [H]as the guidance helped resolve their most important questions?

Crypto Mom: [No]

Budd: So last question, when can market participants expect and exhaustive overview of the law so that they can get the regulatory certainty required to continue to innovate and create American jobs.

The world keeps spinning while the SEC ensures America falls behind

But sound bites won’t change Commission practice. The Telegram SEC fight is only a symptom. Indeed, the SEC embodies the administrative state run amok—the Machine whose highest priority is turf protection and DC cache. The political and judicial branches must cabin administrative agencies. Or future Americans will be tech colonized by those less concerned about Washington chatter or who retires to an Ivy League teaching post.

The majority talkers—academics, policy pushers, and regulators (Nannies)—played their part as innovation hurters, capital killers, and job jerkers. Startups, say the Nannies, must go through them for the privilege of driving the economy.

The SEC Investor Advisory Committee is typical Washington—formed through Dodd-Frank, a political overreaction to a downturn the government itself helped create. It holds hearings and recommends solutions to problems that may not exist to commissioners who may not read them. Its purpose is appearance and to provide some insiders a sinecure. The SEC Investor Advisory Committee is staffed with well-meaning academics and agitprops who never work where they play. But sincerity does not obviate uselessness.

Nannies and Doers presented different ideas about capital raising

Everyone knows capital-raising rules are unforgiving and prolix. And they limit the best prospects to the already moneyed. Thus, two solutions: (i.) allow everyone to invest in riskier but higher reward early-stage companies; or (ii.) force everything into the public markets or die.

The Nannies, Boston College professor Renne Jones (a veteran of such panels), policy hack Tyler Gellasch, state bureaucrat Andrea Seidt, knew the answer. Each spoke of rules, rules, and oversight. None ever signed the front of a business check. None ever will.

Worst was Mr. Gellasch, the neo-New Dealer. In a bygone era, his likeness walked confidently behind Rexford Tugwell or Henry Morgenthau. Full of bravado, confidence, and self-assured in his ignorance. The only thing missing were the wingtips and zoot suit.

Gellasch was the guy 90 years ago telling Americans he could fix things; he and his pals were the smart ones. So smart, it turned out, they took an 18-month downturn and made a 10-year calamity. And left us with a permanent bureaucratic ruling class as the tax we pay for being Americans.

The Doers gave the SEC Investor Advisory Committee needed insight

Standing apart were angel investor Catherine Mott, and compliance CEO Sara Hanks (the Doers). The difference between the two groups is stark. The Nannies look at reports, attend conferences, and think of new ways to control those they study and regulate.

The Doers think in ideas. How to solve problems. This is hard work. Entrepreneurs give their lives to work, knowing the odds aren’t good. Some spend years at or near bankruptcy before success. Gains bring the Nannies’ watchful eyes. The Nannies never know failure (or success) because they never try. Their realm is not ideas but rules and rulers, and obedience to both.

Ms. Mott’s testimony was compelling. She fights the geographic opportunity gap. What happens when a Western Pennsylvania factory shutters? Can a Mississippi startup get a chance with current rules? Right now, Ms. Mott says no. The morass of rules and the zeal to enforce them overpowers outsiders. The money, says Ms. Mott, is looking elsewhere and America loses as a result.

Entrepreneurs get tripped up by regulations and can lose the opportunity to create an impactful enterprise. Harmonization of rules in a balanced fashion can facilitate innovation in the United states. When all net new jobs in the United States are created by companies five years old or less it behooves us to pay attention to the issues for real economic development purposes. Furthermore, China has gained significant ground at a remarkable rate in advancing innovation and encouraging capital investment in startups. The United States is falling behind.

Investor Advisory Committee gives short shrift to the difficulty following SEC rules

Ms. Hanks runs a company that helps startups with rules but even she gets flummoxed. Speaking of solicitation: “Nobody knows what it is, nobody can work out what the rules are. We waste so much time trying to comply with it when we should be trying to work out what information people need at the time of sale.”

Later she defended the much-maligned Reg A+ after Gellasch (of course) insisted it wasn’t working:

I just want to defend Reg A. So, the listing companies right now when I counted this morning there was nearly 600 filings that have taken place under Reg A. Some of them did not qualify because they were crappy. Some of them withdrew because no one was interested in investing because they were crappy and that’s the way the markets work. Of the 600 or so, roughly 6 went to the listing markets and they didn’t do well and a lot of this is because of let’s say optimistic pricing. A lot of it is the whole process and some of these companies may not have been ready to become fully listing companies.

But to take that half dozen and say that’s your data point for disaster or not is to ignore an enormous number of companies who have really nice business plans, who have managed to raise some funds and employ people and are eventually going to come to the public markets we hope. . . . So, I think it’s a little unfair to take a whole category of companies and say they’re all disasters based on the performance of six companies.

Despite what SEC Investment Advisory Committee Nannies say, the private markets are working

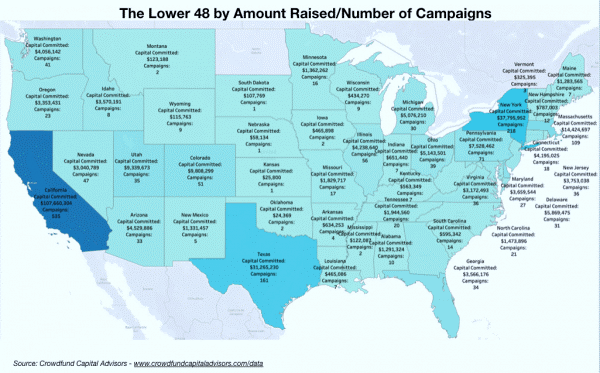

America’s private markets are the envy of the world, accounting for $2.9 trillion dollars in investment last year.

Source: Committee on Capital Markets and Regulation and Voya Investment Management (October 2017) via John Finley, Senior Managing Director & Chief Legal Officer, Blackstone

The Nannies hate this because private raises avoid the compliance cabal, quarterly reporting, activist shareholders etc. Being a public company is hard and costly, that is why there are fewer of them. But the U.S. economy is doing fine. If the Nannies succeeded there would be less startups, less jobs, less investment. But more lawyers, accountants, and regulators. Many companies, especially those not in California, New York, or Massachusetts lose out.

By adumbrating their position, the Nannies entrench those who can afford the public play and keep others with better mouse traps out. It is an academic version of regulatory capture.

What the capital markets need is an open playing field in the private world and acceptance the 1950s economy is gone. Instead of forcing companies into markets where they cannot win, laws should help startups raise small-dollar private money to prove viability.

Whatever happens the economy will not move forward with the Nannies haranguing the Doers.

The Telegram SEC fight over its proposed “Gram” release could mark a sea change for U.S. crypto law. Both sides have dug in amid rising tension. And given the stakes—$425 million in U.S. investment—a truce seems doubtful.

The SEC got an emergency order to stop Gram purchasers “flooding” the U.S. market by reselling Grams to retail investors. Because the commission argues Grams are securities, resales violate U.S. law. But Telegram says Grams are would-be commodities once disbursed via its TON Blockchain. And the fight has turned nasty with Telegram accusing the SEC of “steamrolling” and the commission demanding swift discovery. Without a resolution this case will go to trial and then appellate review. Indeed, this could clarify crypto law rules heretofore dictated only by SEC fiat.

Telegram SEC fight evolved from app’s jump from messaging to blockchain

Telegram’s Messenger is an encrypted app with 300 million

monthly users worldwide. Privacy focus made it a crypto favorite with 84%

of blockchain projects having channels. But it has also become a government target.

Founder Pavel Durov left his native Russia in 2014 after clashing with its

government. And Russia banned

Messenger over concerns of use by state enemies.

Early last year Telegram raised capital for the Telegram Operation Network (TON), “designed to host a new generation of cryptocurrencies and decentralized applications, at a massive scale.” And Telegram sought to power TON through its huge user base and crypto popularity. Heavies scooped up Gram futures contracts deliverable after the blockchain buildout. As a result, Telegram raised $1.7 billion from investors discounted from projected market yields.

Are Telegram SAFTs the same as Telegrams Grams? SEC says Yes

The legal issues embody the crypto conflict. Telegram sold Simple

Agreements for Future Tokens (SAFT) to accredited investors using Regulation D. Both sides

agree SAFTs are securities. But what of Grams themselves? The SEC claims the

SAFT sale began an illegal offering. Under this theory, no separation exists between

SAFTs and Grams. This is a regular capital raise because some money went to

improve Messenger, the TON Blockchain wasn’t finished, and Grams can’t buy

anything yet because would-be products don’t exist.

Thus, the SEC Howeys Grams as “investment contracts.” Thus, they are securities because of profit potential for resellers whose value depends on the skill of Telegram’s team.

Or in SEC speak:

A reasonable purchaser of Grams would view their investment as sharing a common interest with other purchasers of Grams as well as sharing a common interest with Defendants in profiting from the success of Grams. The fortunes of each Gram purchaser were tied to one another and to the success of the overall venture, including the development of a TON “ecosystem,” integration with Messenger, and implementation of the new TON Blockchain.

Telegram

insists it followed the rules by only selling SAFTs to accredited investors.

Grams themselves are a commodity like “gold, sliver, or sugar.” “SEC’s actions hinge

on a fundamentally flawed theory that Grams constitute a ‘security’ subject to

U.S. Securities laws—a theory that runs counter to longstanding Supreme Court

precedent, the SEC’s own views relating to other Cryptocurrencies, and common

sense.”

The SEC Telegram Emergency Injunction forestalls Telegram’s best argument

The preliminary injunction forestalled Telegram from arguing

what it wanted. If initial purchasers resold Grams to “highly interested” retail

purchasers, Telegram could say decentralized occurred via the ‘Hinman

Doctrine.’ And like Ethereum is now beyond SEC reach. This doctrine is named

after SEC Corp Fin Director ‘Bill the Butcher’ Hinman but has no

judicial grounding.

Thus, the SEC Catch 22. To claim decentralization, tokens must be widely distributed and used. But users can’t distribute them unless an open market exists. And an open market can’t exist under securities law. Indeed, issuers can’t even give them away for the desired decentralization.

The SEC knows this:

Defendants knew, however, that to actually implement the TON Blockchain in the real world, the project would require “numerosity”: a widespread distribution and use of Grams across the globe. Indeed, by definition, the TON Blockchain can only become truly decentralized (as contemplated and promoted in the Offering Documents) if Grams holders other than the original Grams purchasers actually stake Grams and, thereby, act as “validators” of transactions on the TON Blockchain.

SEC demands Issuers use Reg A+ . . . Or be Ethereum

The commission’s only apparent answer to this puzzle is to get

Reg A+ qualified like

Blockstack

and wait it out (or be Ethereum). But if

the SEC enjoins the token release that’s it because absent court findings it

has all the power. And as Crypto Czar NPC

Valerie has stated, they

like it that way.

Telegram claims it spent 18 months “voluntarily engaged with, and solicited feedback from, the SEC regarding development and planned launch of its decentralized blockchain platform . . .” And it produce thousands of documents and answered endless inquiries. But when the time came, it didn’t even get a warning an ex parte emergency injunction was coming.

SEC needs judicial oversight or more Crypto Moms

Without court findings this untenable situation will persist.

Commissioner Hester Peirce aka Crypto

Mom discussed a utility-token carve out in recent

congressional testimony. But current commission makeup makes this unlikely.

Telegram has a better fact pattern than Kik having only sold to accredited investors. And it imbued its SAFT with a restrictive legend. Unlike Kik, however, it doesn’t seem to have the stomach for a long-term fight. But it may not have a choice short of rescinding a third of its raise and leaving the U.S. market. Whatever happens here court clarity must happen. The SEC cannot always sit as judge, jury, and bankrupter.

SEC bugles sounded retreat as Enforcement Division troops let Block.one escape an ICO fate that felled lesser transgressors like ICOBox and Munchee. Perhaps it was gearing for heavyweight battles against Kik and Telegram, perhaps Block.one’s lawyers had nude selfies of Chairman ‘Shallow-End Jay’ Clayton.

Whatever the reason, Block.one walked away from a $4 billion

unregistered securities offer with a “stunning

and historically significant” $24 million wrist slap. No disgorgement, no rescission,

no

nothing. It can even keep selling securities (they promise to follow

the rules next time). Block.one and their China-heavy EOS blockchain, the seventh

largest by market cap, celebrated. Others scratched their head. Whether justified or not the SEC’s sudden soft

touch raises questions about favoritism as yet another indecisive year for the token

revolution starts to close.

Block.one’s settlement is either prudent or corrupt

We can view Block.one’s settlement two ways. The charitable

view is the SEC kept its powder, fining an amount roughly

equal to US investment in its raise. Block.one claims it tried to stymie US

investors with IP blocking software and contractual disclaimers. Importantly

though, Block.one marketed the raise here and more importantly the tokens

became instantly tradeable in the U.S. in July 2017.

One cynical conclusion to draw, then, is that the crypto startup community is now following the same norms as the Wall Street banks it seeks to dislodge. Here too, it seems, money buys protection, if not from the law per se but from the impediments to business that adverse rulings have on those of lesser means. It’s a melancholy thought for those who want this technology to lower barriers to entry and give scrappy garage-based startups a chance to change the world.

By this view the SEC’s dreaded storm troopers trade in swords

for plowshares depending on the size of lawyer billables and zeros in the raise.

(Think the crypto version of the government ignoring a presidential candidate’s

official communications placed on a bathroom-based server).

At the least the SEC makes no secret it expects you to dance

to its tune. As Shallow-End

Jay stated in recent Congressional

testimony: “Our doors are open to talk about these things and if somebody’s

going to launch something without coming to see us first, I think that’s a bad

idea.”

Flatter the bureaucrats and the ‘facts and circumstances’

fall your way. Fight it and plowshares sharpen and cannonades besiege your

company. Unfortunately, without bright line rules the SEC leaves for its discretion

who gets artillery and who gets paroled.

The SEC treated other ICO raises much harsher than Block.one

Questions arise because of seemingly disparate treatment with Kik, Munchee, ICOBox, and the looming Telegram. The Kik-SEC battle is the marquee showdown. Commentators describe Kik as belligerent and “angry,” whilst Block.one was helpful and accommodating. But that confrontational stance may provide clarity on issues like decentralization that demurred cases like Block.one will never solve. As the SEC’s infamous token guidance indicates, clarity is not a commission priority.

Unlike Block.one, Kik

raised a comparatively paltry $100 million, half of which was an ostensibly

legal Reg D and by

its count only $16

million from its allegedly illegal token sale. Yet Kik

hasn’t danced the SEC’s tune and is besieged.

The stakes are high. An appellate court could weaken the SEC’s hand and force

them into clearer rules.

The SEC also iced ICOBox. And it

stopped Munchee

on Day Two of its raise. Just last week it filed an emergency injunction to stop

Telegram from flooding the U.S. market with what it deems unregistered

securities. Block.one got none of this despite selling 900 million ERC-20

Tokens the commission deemed unregistered securities. These tokens were

“traded and widely available for purchase on numerous online trading platforms

open to U.S.-based purchasers throughout the duration of the ICO.”

Ask LeBron James and Steve Kerr about kowtowing to China

Whatever underlies the settlement, the commission could have

picked a more sympathetic startup. Block.one’s EOS blockchain is weighted with

Chinese whales and fears

of state intervention abound. The biggest EOS feature is delegated Proof of

Stake allowing China-based nodes to control governance. There is also

wide-spread vote buying.

Given ongoing controversies with Huawei, the NBA, and Hong

Kong, killing Canadian-based

Kik whilst nerfing Chinese-heavy Block.one was not politic. Russian-created

Telegram will now amass even more scrutiny.

The Securities and Exchange Commission’s (SEC) commissioners

testified last week to the House Financial Services Committee. The otherwise

nondescript 3.5-hour

confab briefly surveyed the crowdfunding and crypto landscape. But Congress

missed a huge chance to examine the commission’s scattershot guidance and

arbitrary enforcement. Its desultory policymaking hinders the economy and harms

those it seeks to help.

This hearing followed one on the supposed

menace of private capital markets. But unlike there, Commissioners provided

balanced testimony. And only Robert J.

Jackson Jr.—who (*eye roll*) holds five Ivy League degrees—promoted extreme

anti-capitalist views.

SEC progress on Reg CF crowdfunding could rescue drowning exemption

The hearing began well with Patrick McHenry (R-NC) chastising

Reg CF’s shackling.

McHenry: One exemption that warrants modernization is the crowdfunding exemption. My original crowdfunding bill which was included in the JOBS Act was only a few pages long, 11 pages in fact. I appreciate the SEC and their hardworking staff creating 685 pages worth of regulations around those 11 pages. The absurdity of this I have pointed out a number of times since then. So, you’ve given me at least the rhetorical value of talking about the burden of SEC regulation of making an exemption and a public law completely meaningless because of the impact of the costs.

As the bill’s sponsor, however, his concern proved sadly

unique as the hearing wandered about. Everyone knows Reg

CF’s shortcomings. And the commission seems finally to be acting.

Chairman Shallow-End Jay Clayton: You can get up to a million-dollar company going with Reg Crowdfunding and some of our other exemptions. It’s really hard to grow a business from say a $1M business to a $50M business . . . if there are things that we can do to facilitate capital formation in that gap so our small businesses can become larger I think that’s an area we should focus on.

The SEC recently sought public

comment on reconciling and improving the private exemptions. Commenters sent

many good ideas. Long awaited action is hopefully afoot.

SEC token and crypto guidance remains woeful

Less promising is token-sale progress. The SEC seems no

closer to solving the crypto riddle than during the ICO

craze, with one exception.

Congressman McHenry mentioned the Blockstack

Reg A+ token sale and several are irked by Mark

Zuckerberg’s corporate crypto scheme. But commissioners couldn’t remove

crypto uncertainty. Commissioner Hester Peirce, aka Crypto

Mom stated such when discussing utility tokens and policy-by-enforcement that

only seems to bother her.

Crypto Mom: I would like to see us be a little more forward thinking in ways that we might accommodate unique aspects of digital assets. For example, digital assets that are utility tokens I don’t know that the securities laws framework that we have right now is the appropriate framework for them and so I’d like for us to think about creating some kind of safe harbor.

Crypto Mom: But enforcement is a poor way to announce policy. We need to be clear in writing our rules and we need to make sure we provide the guidance that firms and individual need as necessary. We understand that our rule book is complicated, and we work with well-intentioned firms and individuals to help them comply with our rules.

The SEC’s April Digital Asset “guidance”: dazed and confused

Budd: In April Fin Hub published a framework for investment contract analysis of digital assets which included 60 plus factors for determining whether or not the SEC would consider a digital asset a security. In a statement released alongside your framework your colleagues Bill Hinman and Valerie Szczepanik indicated that the framework is not intended to be an exhaustive overview of the law. But rather an analytical tool to help market participants . . . [H]as the guidance helped resolve their most important questions?

Crypto Mom: [No]

Budd: So last question, when can market participants expect and exhaustive overview of the law so that they can get the regulatory certainty required to continue to innovate and create American jobs.

The SEC plagues entrepreneurs with ambiguous and arbitrary enforcement

The Commission’s name brand, massive budget, and economic power

incentives risk-averse,

snails-pace progress on issues that won’t wait.

Indeed, the SEC abstains from the only recent securities

success: Reg D. Onerous

rules knifed Reg CF

and Reg A+. And rules

encourage companies to stay private rather than face the many IPO burdens.

All the while, former SEC

staff and commissioners

get massive paydays to interpret and cajole because no one can discern motives

behind mountains of disclaimers and subpoenas. Staffers justify this as needed

“flexibility.” As

NPC Valerie Szczepanik noted, “The lack of bright-line rules allows

regulators to be more flexible.”

This is true but has other effects. It leaves regulators with massive discretion. And it gives them enormous power over the economy with no responsibility for the results. It mandates entrepreneurs approach them hat-in-hand for permission. And it makes them sought after speakers on the conference circuit.

But it’s a zero-sum game. Every unit of power Ms. Szczepanik reserves for herself and her colleagues removes it from job producers. Indeed, every ambiguous pronouncement shunts billable hours to lawyers and compliance professionals instead of research or marketing. Those building tomorrow’s economy need the flexibility not bureaucrats. They will power our future long after Ms. Szczepanik takes her professorship or retires to a nonprofit.

Congress missed a chance to examine the SEC’s misguided de facto policymaking

Entrepreneurs facing intense market pressures need flexibility.

Warren Davidson’s (R-OH) soliloquy struck the matter and is worth fully quoting:

Davidson: Recently director of corporation and finance Bill Hinman stated in a fireside chat that the SEC prefers an approach to digital assets through facts and circumstances rather than a bright line test. This company by company approach prevents regulatory clarity and it suffers from some of the charm and inefficiency of third world power structures. For this reason, although innovators are in America and innovation is still occurring in America capital is fleeing. Not to avoid our regulations to find efficient regulatory clarity. And they’re finding it elsewhere. We need a simple set of rules that apply equally and clearly to all. That is the premise of a bill I know you won’t talk about. But the framework that the market needs. Where is the capital going? Places like Singapore, the UK, Switzerland, have laid out clear frameworks for digital assets.

Meanwhile the US hundreds of companies await No Action Letters, with only two having been issued thus far by the SEC. Now I agree with you that the ICO situation represents bad outcomes, but the root issue remains. America does not have a clear regulatory framework. Consumer and investors are harmed by that status quo in fact Commissioner Peirce nailed the explanation, the SEC should not only be concerned about fraud but also about opportunity. Our failure to provide regulatory clarity fails Americans on both counts. We have become the world’s land of opportunity the best destination for goods, services, capital, intellectual property and more by anarchy or by inaction. With respect for digital assets it’s time for deeds not words.

But too often we get years-long dithering before eye-rolling

guidance or subpoena floods. And people never subject to market forces live

comfortable lives in prestige whilst hindering tomorrow’s economy.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

A cookie is a string of information that a website stores on a visitor’s computer, and that the visitor’s browser provides to the website each time the visitor returns.

THECROWDFUNDINGLAWYERS.COM uses cookies to help identify and track visitors, their usage of THECROWDFUNDINGLAWYERS.COM sites, and their website access preferences. THECROWDFUNDINGLAWYERS.COM visitors who do not wish to have cookies placed on their computers should set their browsers to refuse cookies before using THECROWDFUNDINGLAWYERS.COM’s websites, with the drawback that certain features of THECROWDFUNDINGLAWYERS.COM’s websites may not function properly without the aid of cookies.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.