Reg A+ real estate funds? RICO Litigation Support? Stranger Things house rentals? YouTube advert revenue shares? Oh My! These were just some of the emerging investment types discussed in the recent webinar, ‘Beyond Equity: Novel and Emerging Investment Types for Investors.’

The panel featured Paul Lovejoy, a financial advisor and prolific Reg CF/Reg A+ investor, and Scott Kitun, Chief Business Officer at GigaStar (a Reg CF platform enabling investors to participate in YouTube creator revenue share offerings), and Allison Miettunen, an experienced Business Consultant with a demonstrated history of working with startups in the FinTech industry.

As the panelist discussed, Reg CF and Reg A+ are clearly evolving past the conventional SAFE or convertible note into realms unimagined during the 2012 JOBS Act debates. The once-scorned exemptions are having their moment as alternative capital sources and investment opportunities continue to emerge.

Beyond Equity – Reg A+ as fund asset manager

Reg A+ is now going deep into real estate. Unlike Reg CF, issuers can create funds from Reg A+. According to Paul Lovejoy, the portal FundRise was the first to create this structure. This instrument can have the benefit of producing steady income over time whilst also broadening the investor pool to the general public.

Lovejoy also discussed a Reg CF instrument that acted as Reg A+ support for litigation against private equity that had a RICO element–something unfathomable during the Congressional Reg CF debate and investing in rental income from the ‘Stranger Things’ home.

Beyond Equity – Reg CF and the creator economy

Even more interesting was what Scott Kitun at GigaStar is doing with YouTubers. These creators are selling parts of their ad revenue to a Reg CF crowd. Investors own part of a production with almost no infrastructure costs, get steady revenue, and support their favorite creators. Creators use this capital to build out their personal empire with merchandise, additional channels, or anything else. Smart investors can capitalize on emerging fashionable trends. Rev Shares produce quick returns, aided by an enthusiastic investor crowd whose payouts align with channel success.

Further, tokenizing these rev share instruments and placing them on Alternative Trading Systems (ATS), allows for greater liquidity–a constant irritant for Reg CF equity investors. As these Reg CF security tokens evolve, smart contracts will initiate instant payouts to all investors based on their investment percent.

This industry is still nascent and there is a ton of money to be made. As Kitun explained, “The creator market has grown 10x every three years It’s a $250 billion dollar market right now, it will be a half a trillion dollars by ’28, it will be probably a trillion by ’30 at that pace, maybe more.”

The coming economic reversion

As the world becomes more decentralized and the traditional cultural gatekeepers in media, entertainment, bureaucracy, technology, finance, and corporations fall to the crypto revolution (the subject of my upcoming book) the business landscape will change. Prior to the consolidations that happened in the late 19th century, most people worked as entrepreneurs or in small firms.

Aided by these changes in the securities laws, we are on the cusp of an economic reversion, where many people work for themselves or in small groups. But this time their communities will be global. Those interested in participating or profiting from this transformation should look at the exciting economic revolution Reg A+ and Reg CF are leading. *Not Financial Advice*

Heavyweights in the Reg CF industry including Crowdfund Capital Advisors (CCA) and the Crowdfunding Professional Association in conjunction with Building Legendary Professional Networks, a national professional network representing a broad cross-section of the life science ecosystem. These groups have requested the Securities and Exchange Commission (SEC) to raise the Reg CF offer limit from $5M to $20M with automatic indexing for inflation.

If the SEC moves forward with a proposed rule it would reflect the growing acceptance of Reg CF as a viable exemption. It has now provided over 8,800 issuers more than $3.2B in capital. This success contrasts with the Reg CF faced hostility during its implementation in 2016. After four years relatively fraud-free years, the Commission raised the limit from $1M to $5M in late 2020.

Startups have benefited from raised offer limit

CCA provides statistics backing it’s proposal for the next offer-limit raise.

40.3% returned to the Reg CF market for follow-on offerings

20 months was the median time to first follow-on—consistent with normal business growth cycles

$3.1 million was the median additional capital raised after hitting the cap

$214+ million has been raised in aggregate by issuers who initially maxed out

29.4% of these companies raised at least $1 million more in subsequent Reg CF rounds

CCA states the proposed limit would allow fast growing companies to jump into Series A or low-level Series B “while keeping the existing disclosure, intermediary, and investor-protection framework fully intact.”

It would also likely retire the under utlized Reg A+ Teir One. Between the Tier One and Two, Tier Two accounts for 89% of the issuers and over 96% of the capital raised despite heavier ongoing compliance obligations. A $20M Reg CF limit would solved Reg A+ Tier One’s biggests deterrents: no state regulatory review and the ability to raise from multiple states.

SEC Encouraged to Raise Reg CF Offer Limit – Benefit to Retail Investors

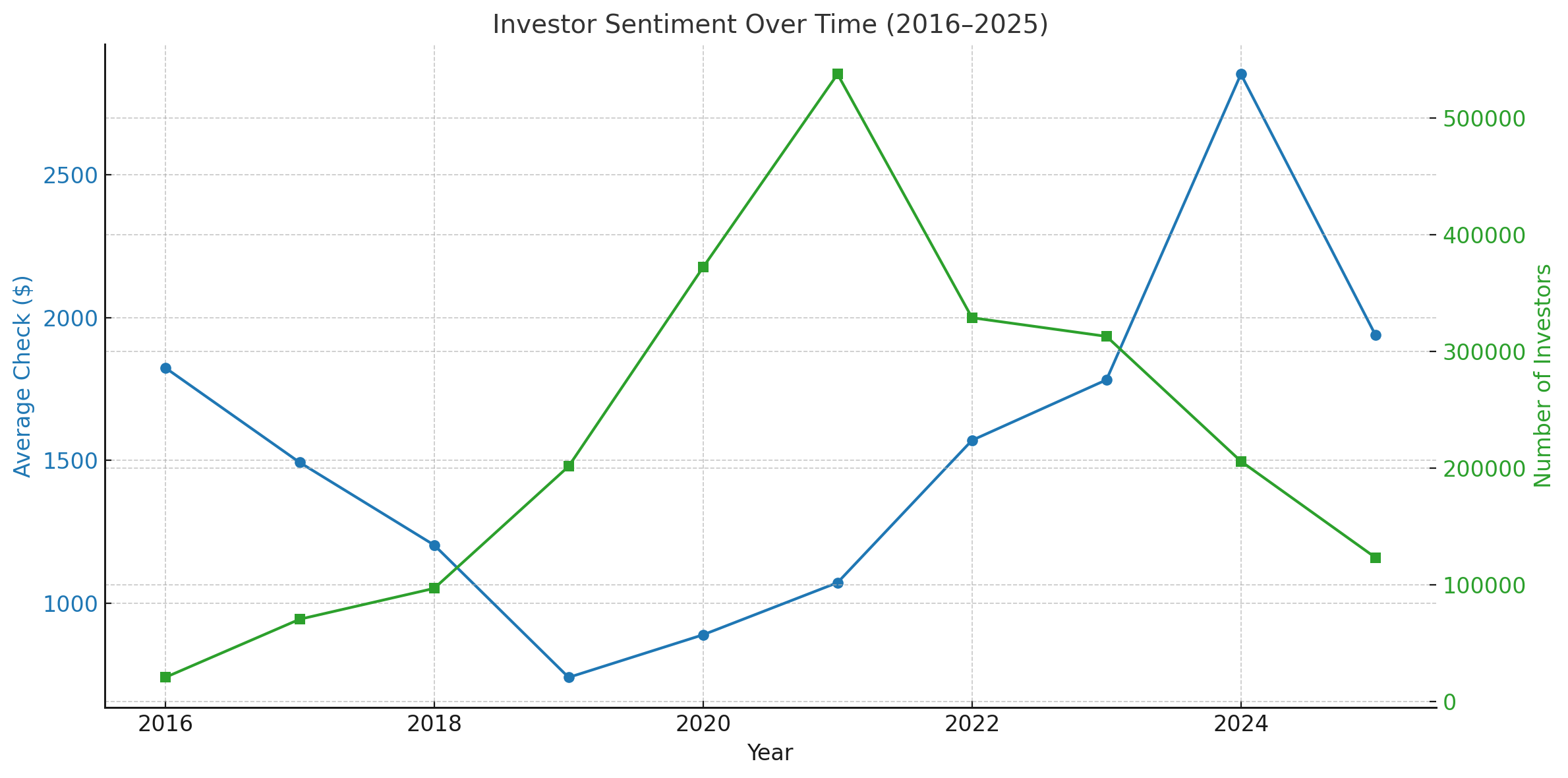

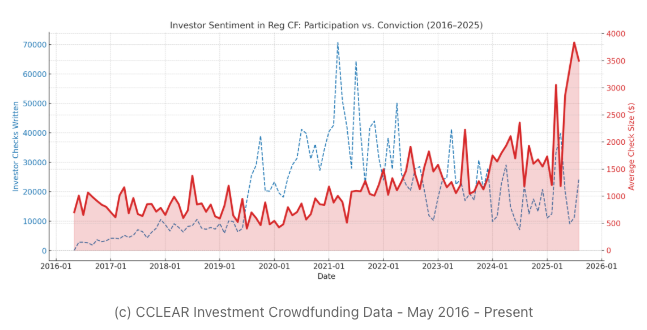

Reg CF’s maturity is evidenced paradoxically by fewer companies utilizing it. In the post-COVID of stimulus checks and cabin fever, companies flooded the market, many lacking sound fundementals. Now fewer companies raise this way but the ones that do bring in much bigger checks.

Source: Crowdfund Capital Advisors

The reason is more investors and companies see Reg CF’s inherent advantages:

• Broaden your investor base: Unlike other funding models, Reg CF can diversify your investor base from both a financial and geographical standpoint. Portals can accept investors from anywhere in the US, giving your business a potential foothold in all 50 states.

• Turn your customers into marketers: Reg CF allows your customers to become financially invested in your business and see their investment grow as your business grows. This provides a free marketing campaign for your business with every new investor.

• Incentivize your investors: Reg CF allows you to provide perks as part of the investment. Depending on the product this could include the product itself, ‘founder’ status on your website, access to events, or anything else that may induce an investment.

• Prove value to institutional investors: A successful Reg CF raise can show larger, institutional investors your business is ready for the big money. Many larger investors are now requiring “social proof” of a company’s business model. Your business can show larger investors value and momentum and provide your business “bridge money” while larger investors evaluate your model.

The SEC should act on this proposal and further intergrate investors, marketers, and customers.

The numbers are in! Whilst COVID-era “irrational exuberance” has subsided, the Reg CF market continues to grow and mature. Stimulus checks may have encouraged loose spending, but Reg CF companies are now worth more and are receiving bigger checks. These trends will likely continue as the predicted economic effects of the “Big Beautiful Bill” take effect.

From its start a decade ago, Reg CF has risen from maligned step-child to private-market budding star. According to Crowdfund Capital Advisors, (CCA) which curates Reg CF data, the exemption has “quietly become a $3.2 billion market.” This includes around 10,300 offerings with almost 7,200 reaching their targeted minimum.

CCA curated this list to exclude “one-offs,”–like movie projects and real estate, parallel Reg D offerings–and ended with 4,358. Incredibly, 85.1% are still operating. A success rate that far outstrips the know-it-all VCs.

Reg CF Outlook Bright for 2026 – Valuation and Raise Amounts

One of the signs the Reg CF market is maturing is through valuation. According to Kingscrowd, the total valuation of companies raising through the Reg CF is $17.2 billion up from $16.3 billion in 2024–a 5.5% increase. The average valuation during this period was $40 million, a number unheard in the early days and a 6% increase from 2024.

Raise amounts also augur a bright 2026. In December 2025 Reg CF companies raise $26.1 million up a whopping 18,7% from December 2024.

Reg CF Outlook Bright for 2026 – Declining Offerings, Bigger Checks

Critics may point to the declining number of Reg CF offerings to aver all is not rosy. It is true, that number of offerings has decreased since the stimulus-induced craze earlier this decade. But that fact comes with a flip-side. The average checks are getting bigger, now totaling around $3,500. This means less fly-by-night and more scrutiny per offering. Investors reward issuers that pass the test with bigger checks and the loyalty and enthusiasm that tethers. Bigger checks means more due diligence and greater peace of mind for the smaller investors along for the ride.

Source: Crowdfund Capital Advisors

What the maturing Reg CF market proves is Jossey PLLC‘s slogan. Owners and executives can “turn their companies into movements”– fewer raises, but more successful companies, with more loyal customers, and organic marketers. Given the expected economic tailwinds, this year should be a banner year for Reg CF. And the market will only continue to strengthen.

By Jossey PLLC – Turn Your Company Into a Movement!

Real Central NJ, the hottest soccer team in central Jersey, which is working toward becoming the area’s only professional soccer team, has launched its Reg CF Testing the Waters campaign. Interested potential investors can go RCNJ’s Wefunder page to express interest in getting in early. This is a rare chance to own part of a team on track to become professional in 2026!

Real Central NJ is currently “testing the waters” under Regulation Crowdfunding. No money or other consideration is being solicited or will be accepted, and no offer to buy securities can be accepted until an offering statement is filed and made available through an authorized portal. Any indication of interest is non-binding.

American Icon Brewery, Vero Beach’s hottest gathering just launched their Reg CF crowdfunding campaign. Investors can not only get potential returns but become a part of the new immersive “Brew Haus” experience the owners are creating in one of Vero Beach’s most iconic destinations!