Franchisors looking to expand into new markets and franchisees looking to “take the plunge” often face a dilemma: where to get the upfront capital. Franchise attorney Schuyler Reidel recently explored some traditional ways franchisees broach this issue. They include Franchise financing programs, loan guarantees, working capital loans, royalty fee deferrals, franchise associations, SBA loans or alternative investment networks.

All these methods have helped entrepreneurs begin their franchise journey. But another method has recently emerged that may overtake all past avenues for the added benefits both franchisors and franchisees get in publicity and more intense customer loyalty. This new method is Regulation Crowdfunding (Reg CF).

Reg CF is a set of regulations created by the Securities and Exchange Commission (SEC) deriving from Title III of the JOBS Act of 2012. Although passed into law over a decade ago the regulations did not go live until 2016. In 2021, the SEC modified the rules making them more founder and investor friendly.

Reg CF allows anyone to become an investor in a small business or startup, this includes franchises. (Publicly traded companies such as McDonalds are not eligible). Investors buy the securities over funding portals or traditional broker dealers. The securities can cover a wide range of financial instruments from equity, to future equity, to traditional notes, and profit-sharing “rev shares.”

Franchisors who have established customer bases are well suited for these types of raises given their consumer-facing businesses and the ability for the company (issuer) to include coveted perquisites thematic to the raise.

Reg CF crowdfunding allows franchisors and franchisees to collaborate on capital needs

Here are two scenarios where the franchisors and franchisees can benefit from a Reg CF raise:

Scenario One

An established BBQ restaurant with a loyal following wants to add two more stores. The total capital needed is $1.2M. They hire an attorney, contact a portal, get the required financial review completed and eventually go live with their raise. In the meantime, the owners reach out to their customer base to “Test the Waters” and gauge interest in the raise. They receive an enthusiastic response. When the raise goes live investors learn their investment entitles them to other benefits depending on their investment level including free T-shirts, “comped” meals, and the opportunity to attend a private dinner with the owners after the grand opening. After three months the raise closes and six months later the owners have two new stores.

Scenario Two

A pizza franchisor discusses a franchisee deal with two young entrepreneurs. The potential franchisees are eager to get into the business but do not have the $500k of upfront capital required. The franchisor allows them to use the company’s marks and email list in a Reg CF campaign. Because the raise will be imputed to the franchisor, the security is structured as a “rev share.” That way, the franchisor will not sell any equity in the company. Instead, the franchisees will finance the upfront capital by promising a part of future profits to the investors.

The franchisees hire an attorney, set up an LLC, and conduct the raise through a broker dealer with the franchisor’s blessing. The franchisor brings his customer base “closer” to him by making them investors and not just customers. The customers feel more aligned with the pizza franchise as investors and eat there more often. After four months the franchisees secure the capital needed to open the store. Two years later they have paid off the investors and start the process over for their next store.

*All investment comes with risk; these scenarios are for information purposes only.

Reg CF will upend capital raising for franchises

Reg CF is the future in franchise capital. It allows franchisors the chance to expand their business in a way the promotes brand awareness and loyalty. Franchisees looking for upfront capital may be able to use the franchisor’s goodwill and tap into their existing customers to create an investor base.

For more information on starting a franchise contact Schuyler Reidel at [email protected]

For more information on Reg CF raises for franchises contact Paul H. Jossey at [email protected]

In May, Regulation Crowdfunding (Reg CF or equity crowdfunding), an innovative law that opened the private capital markets to everyone, turned seven years old. In this short time, it has gone from regulatory stepsibling to regulatory success.

The journey has not been smooth.

From its start in the JOBS Act of 2012, critics including state and federal regulators, associations, and some politicians, attacked equity crowdfunding as an unwise and unneeded tool that would attract scammers whilst leaving John Q. Public holding the bag.

Indeed, the Securities and Exchange Commission so opposed Reg CF it took four years to produce the regulations, heaping loads more issuer requirements.

The SEC eventually saw Reg CF as a regulatory success

But after four years of relatively smooth sailing the SEC reversed course. In 2020, it acknowledged the predicted fraud tsunami had not occurred and loosened the rules, making the Reg more investor and founder friendly. This combined with rising interest in online investing because of the pandemic has meant seven years hence, Reg CF has become a regulatory success.

1.7 million investors have invested over $1.8 billion into over 4,100 startups and small businesses across 1,700 cities in the US.

Companies that have successfully raised via Reg CF are now valued at over $60 billion.

Reg CF has contributed approximately $4.7 billion to the overall economy through salaries, inventory, rent, professional services, and various operational expenses.

Besides the raw numbers, Reg CF has performed a social good by allowing entrepreneurs access to capital who were traditionally outside the venture capital pipeline. According to CCA, “women and minority entrepreneurs (that routinely struggle to access capital) have had greater success within Investment Crowdfunding and are raising up to 50% of the capital.”

Securities professionals help keep Reg CF a regulatory success

But Reg CF critics weren’t completely wrong. As with any investment endeavor, there are risks for founders and investors. Founders new to the startup grind may overpromise, choose the wrong security, or fail to disclose material information to investors. Ordinary people investing in startups for the first time may not realize the mechanics of liquidity, valuation, or disclosures. And of course, many startups fail, and investments are lost. If not properly configured, founders could face liability from both investors and authorities. In 2021, the SEC brought its first charges against an issuer and funding portal alleging fraud.

That is why it is so important for Reg CF companies to hire counsel to guide them through the process, file the proper paperwork and advise founders on issues of portal selection, financial instrument, valuation, disclosures, investor communications, and more.

The Reg CF revolution is just beginning. As more companies realize the benefits of democratizing capital raising to include their loyal customers and brand ambassadors, the numbers will keep growing. As younger generations already accustomed to transacting online become founders and investors themselves, the days of wooing Silicon Valley VCs in haughty boardrooms instead of one’s own crowd on Twitter or TikTok may end.

Wherever the Reg CF journey goes, its best days are ahead.

Firm client Zero Cheating has now crossed $500k in commitments in its Reg CF round on the Wefunder platform.

Zero Cheating is a fully automated online proctoring service. I need your investment to stop cheating during online exams. Its lead investor is on the faculty at Yale.

Congratulations Zero Cheating!

Learn more and invest here: https://wefunder.com/zero.cheating

Ben Franklin was a remarkable man. In his life he assumed many roles that won public acclaim, including successful businessman, publisher, inventor, statesman, and revolutionary.

But whilst those roles may be familiar to the public, his role as a fundraiser may not. Ben Franklin helped raise money to create many adored institutions that still stand today including the University of Pennsylvania and the Philadelphia library.

Ben Franklin: master crowdfunder

But one fundraising project he didn’t lead yields lessons for modern startup founders seeking capital. Recounted from his autobiography, after just having successfully raised money for Philadelphia’s first hospital, a Reverend approached Franklin for his help in raising for a meetinghouse.

Franklin, wary of wearing out his welcome through constant solicitation, demurred. The Reverend then asked for his investor list, he again refused on the same grounds. Finally, he was asked for advice, this he readily granted:

In the first place, I advise you to apply to all those who you know will give something; next to those whom you are uncertain that they will give you anything or not, and show them the list of those who have given; and lastly, do not neglect those who you are sure will give nothing, for in some of them you may be mistaken.

After taking Franklin’s advice, the Reverend obtained a “much larger sum than he expected, with which he erected the capacious and very elegant meetinghouse that stands in Arch street.”

Another Franklin fundraising habit was to “prepare the minds of the people by writing on the subject [of the fundraise] in the newspapers.”

Applying Franklin to get more Benjamins

These strategies align perfectly with the modern age. Regulation Crowdfunding [Reg CF] allows founders to raise capital just as Franklin did. To “prepare the minds of the people” founders should “test the waters” or gauge interest in the raise beforehand, by securing pre-commits.

Second, they compile their list of likely and unlikely investors. In modern parlance, these are the founder’s ambassadors: people who believe in the founder, their team, and their company. These ambassadors don’t necessarily have to be big investors. If they are willing to post the raise on their social-media accounts to increase visibility, they are meaningfully helping.

Founders that apply Franklin’s methods by compiling lists, selecting ambassadors, and testing the waters will likely have successful raises, even if they aren’t founding Ivy League institutions or public libraries.

Firm client Musiversal, the world’s 1st remote recording studio and end-to-end music production platform just closed their Reg CF round on the Wefunder platform. The company raised over $330k from nearly 300 investors around the world.

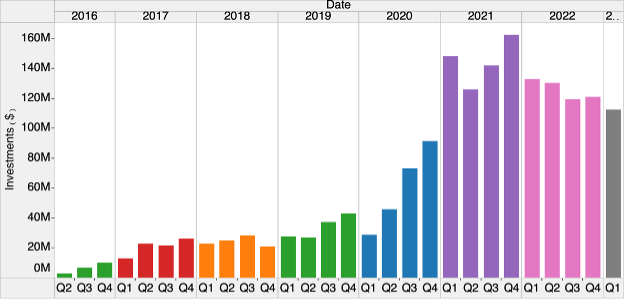

Reg CF Q1 numbers hold steady despite economic turmoil

The New Year has seen bank failures, stubborn inflation, rising interest rates, and pullback from venture capitalists. But financial positions worsen, equity crowdfunding (Reg CF) keeps rising as a preferred capital-raising method for early-stage companies. Although, down somewhat from the COVID boom, Reg CF issuers continue to raise at a healthy clip despite growing economic caution.

Reg CF Q1 numbers continue to show promise

In every economic measure Reg CF issuers enjoyed a steady first quarter to 2023. Crowdfund Capital Advisors (CCA), which curates Reg CF data reports:

[T]he number of issuers coming online was up 0.3% over the prior year and down 1.3% over the prior quarter. 91 issuers ran a follow-on round. Down 9.1% over the prior year but up 16.9% over the prior quarter.

Q1 saw the lowest capital committed since Q4 2020. It was off 15.4% over the prior year and 7.1% over the prior quarter.

The number of checks written was up 32.6% over the prior quarter but down 26% over the prior year. Average check size grew 16.5% over the prior year to $1,688 but fell 29.8% over the prior quarter.

Quarterly median valuations hit an all-time high of $14M. For pre-revenue issuers, median valuations hit a quarterly high of $13.2M, but post-revenue issuers saw a decline to $14M from a high of $15.1M in Q3 2022.

Quarterly funded deals remain high with 290 successful deals in Q1.

The healthy numbers come despite the big money pullback embodied by the Silicon Valley Bank collapse, perhaps the largest bank for venture capitalists. This may bode well for Reg CF according to CCA’s Sherwood Neiss, “This will be the first true test of the industry’s ability to substitute the role of Venture. While the need for Venture Capital will never disappear, a void has been created in the marketplace . . . Now we will see if, in fact, a startup’s community can play the role of VC.”

Source: Crowdfund Capital Advisors

Reg CF Q1 numbers foreshadow longer term and global trends

Over the next few years, crowdfunding will keep trending up. According to Fortune Business Insights, the global crowdfunding market currently valued at $1.41 billion in 2023 and will more than double by 2030 to $3.62 billion.

[T]he COVID-19 pandemic helped accelerate the adoption of crowdfunding as a fundraising method, as $214.9M was raised via equity crowdfunding in 2020, representing growth of 105% from 2019. With many businesses struggling to access capital during the pandemic, crowdfunding platforms emerged as a valuable source of funding, helping companies to quickly and efficiently raise the capital they needed. . . .

This shift towards crowdfunding can also be attributed to the changing investor landscape. Younger generations, such as millennials and Gen Z, have shown a greater interest in impact investing, and are more likely to invest in companies that align with their values and beliefs. Crowdfunding provides an opportunity for these investors to support companies that are making a positive impact, and to have a voice in the companies they invest in.

Reg CF has other other benefits

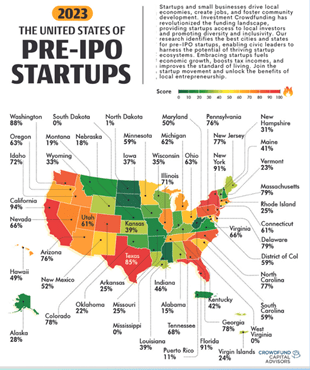

Broaden your investor base: Unlike other funding models, Reg CF can diversify your investor base from both a financial and geographical standpoint. Portals can accept investors from anywhere in the US, giving your business a potential foothold in all 50 states.

Turn your customers into marketers: Reg CF allows your customers to become financially invested in your business and see their investment grow as your business grows. This provides a free marketing campaign for your business with every new investor.

Incentivize your investors: Reg CF allows you to provide perks as part of the investment. Depending on the product this could include the product itself, ‘founder’ status on your website, access to events, or anything else that may induce an investment.

Prove value to institutional investors: A successful Reg CF raise can show larger, institutional investors your business is ready for the big money. Many larger investors are now requiring “social proof” of a company’s business model. Your business can show larger investors value and momentum and provide your business “bridge money” while larger investors evaluate your model.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

A cookie is a string of information that a website stores on a visitor’s computer, and that the visitor’s browser provides to the website each time the visitor returns.

THECROWDFUNDINGLAWYERS.COM uses cookies to help identify and track visitors, their usage of THECROWDFUNDINGLAWYERS.COM sites, and their website access preferences. THECROWDFUNDINGLAWYERS.COM visitors who do not wish to have cookies placed on their computers should set their browsers to refuse cookies before using THECROWDFUNDINGLAWYERS.COM’s websites, with the drawback that certain features of THECROWDFUNDINGLAWYERS.COM’s websites may not function properly without the aid of cookies.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.