Stablecoin market capitalization has risen 500% in past twelve months. The growth aligns with growing interest in transacting outside heavily regulated banking system. People are seeing myriad benefits from stablecoin use including yields from “staking,” more fluid trades, smaller fees, simple borrowing procedures, and smooth cross-border payments among many others.

The Biden administration looks on with alarm and suspicion. Last summer, the ‘President’s Working Group’ (PWG), composed of several financial regulators, announced it would evaluate stablecoins and recommend action. The president should scrap the gloomy report recently issued by the PWG and let the stablecoin market develop.

Because of their value in the crypto ecosystem, stablecoins demand more interest than their dollar-pegged book value, to the benefit of ordinary American savers. Virtual marketplaces like Nexo and Celsius offer 10% APY or higher to deposit stablecoins.

PWG report embodies bureaucratic quagmire

The PWG report ignores stablecoin benefits and instead reflects a myopic, risk-averse, regulator-centric view of crypto that permeates the executive. The dour report warns of every possible stablecoin risk. It suggests Congress create a “comprehensive” regulatory apparatus to oversee the supposed risks and warns it will pursue the matter solo if Congress fails to act. The Financial Stability Oversight Council (FSOC), an administrative board created through Dodd-Frank, could designate stablecoins systematically important thereby subjecting them to onerous oversight, compliance, and enforcement.

Odd things arise from this approach. First it is ironic the administration insists the stablecoin phenomenon is so unwieldly it requires a new regulatory cloak whilst Gary Gensler, SEC Chair and PWG member, has insisted all year the larger crypto space needs no such overhaul as it fits within Howey-investment-contract analysis and many cryptocurrencies are already subject to the SEC’s jurisdiction.

It is curious why this relatively tiny $139 billion market would need a comprehensive solution but the greater the greater $3 trillion crypto market must conform with decades-old investment-contract analysis that Congress never defined in the original statute. The extent of Mr. Gensler’s guidance boils down to enforcement, period. Unsurprisingly, the SEC has stablecoin issuers Tether and Circle in its crosshairs.

PWG report sees risks where they don’t exist

But as the Digital Chamber of Commerce argues, stablecoins, a tiny subset of the overall crypto market, already fit into regulatory apparatus: “applicable regulatory frameworks can involve money transmission laws and state-level trust company charters on the federal level, and FinCEN, CFPB, and CFTC regulations on the federal level.”

This system works as intended. When stablecoin Tether allegedly used shady accounting practices for stating its reserves, both New York state and CFTC levied fines. Now all major stablecoins voluntarily publish their reserves on varying schedules. In fact, Grant Thorton LLC a prestigious accounting firm attests to stablecoin Circle’s reserves.

Second the bureaucratic worrywarts concern about risks, which the report classifies in several distinct ways, is unfounded. The market is not only miniscule compared with the crypto market but other financial sectors as well. As Cato Institute’s Norbert Michel relays, circulating dollars constitute $2 trillion, treasuries $5.4 trillion, money-market funds $4.5 trillion, and equities $40.7 trillion. An FSOC ‘systematically important’ designation would be well disproportionate to its size. In a letter to Treasury Secretary Janet Yellen, Senator Patrick Toomey (R-PA) explains, the Clearing House Payment Company, one of only eight designated systematically important financial market utilities, clears and settles $1.8 trillion payments per day.

Stablecoins are less risky than other assets

Further, stablecoins because of their 1:1 pegs pose less systemic risk than other financial instruments. As the Digital Chamber of Commerce states:

[L]eading U.S.-headquartered stablecoin payments systems – unlike banks – are not leveraged. Instead, the reserves of these stablecoin payments systems are held almost entirely in cash or cash equivalents. And, notably, the only sizable U.S. dollar-pegged, cryptocurrency backed stablecoin is over collateralized. The reserves of these stablecoin payments systems arguably have a much lower risk profile than permissible investments of other state-regulated money services businesses.

Finally, PWG advocacy for “comprehensive” federal oversight, while unsurprising, should be examined by the results of other such federal efforts. Empirical evidence shows the Securities Act of 1933 did little to thwart fraudsters. Dodd-Frank has been worse, with its notable accomplishments being slowing the IPO market, killing off free bank accounts, and destroying money market mutual funds. These laws did no more for financial integrity than McCain-Feingold did to restore trust in campaign finance. The list goes on.

In fact, Congress’ only successful financial reforms have been deregulatory. The Small Business Investment Incentive Act of 1980 led to the wildly successful Reg D. The Jumpstart Our Business Startups Act of 2012, is slowly creating a business-capitalization revolution with Regulation Crowdfunding and Regulation A+.

The PWG should allow stablecoins to flourish and abandon the overbearing regulatory instinct to suffocate innovation it does not understand. If it does this, the stablecoin market will grow and allow ordinary people to prosper from its success.

Helen Hodler and Sam Saver meet, fall in love, and start planning their future. Sam opens a savings account and gets 0.06% APY (interest rate). More adventurous Hellen buys a stablecoin—redeemable 1:1 with a US dollar—and deposits (or ‘hodls’) it with an exchange. She gets 8.88% APY. Our well-heeled financial-policy setters like Federal Reserve Chair Jerome Powell (net worth $55 million), Treasury Secretary Janet Yellen (net worth $16 million), SEC Chair Gary Gensler (net worth $119 million) side eye Helen.

A recent report on stablecoins by the President’s Working Group on Financial Markets outlines official concerns. They think she is too unsophisticated for her choice. They think she and the exchange may pose a systemic risk to the entire U.S. financial system. The report asks Congress to solve these apparent issues but suggests federal agencies will act alone if necessary.

In reality, smothering people with financial bureaucracy brings far greater risks for our nation’s economic prosperity and stability. Instead, the federal government should allow stablecoin issuers, crypto exchanges, and the Web 3.0 revolution it will fuel to flourish.

Stablecoins are working

Stablecoins are already vital to the crypto ecosystem. Before their advent, crypto trades paired with fiat currency. Stablecoins made trading faster, cheaper, and more liquid. Although only widely used since 2017, the market has bloomed, with a current $131 billion capitalization.

People would marvel at the innovations rolling out in this short time if we were unaccustomed to the private sector rapidly solving problems. By comparison, China began working on a digital yuan in 2014 and is only now doing pilot programs. A U.S. government version is years away.

But Hellen need not wait for government to lead the way. She can choose a stablecoin backed by cash and commercial paper, or one by commodities like gold, or one governed by algorithms. She can pick one that attests its backing quarterly, or monthly, or 24/7. The market’s ‘invisible hand’ connotes each coin’s rising or falling fortunes.

Nefarious stablecoins actions have been punished

No human system is perfect. After years of questions about its reserves, , one issuer – Tether – settled with the New York Attorney General’s office over alleged shady accounting. It also paid a $41 million-dollar fine to the Commodity Futures Trading Commission. Yet the market didn’t collapse – it incorporated this information and continued ablaze. As the market matured and new entrants arrived, issuers began attesting their reserves.

All this success outside the government’s “invisible foot” alarms Washington types. Bureaucrats and allied intellectuals worry about investor protection and ‘runs’ to fiat currency. Ironically, one might argue a country $27 trillion in debt has bigger concerns than a smoothly functioning $131 billion market. Nevertheless, they persist.

Gary Gensler is the stablecoin killer

Under the guise of technology neutrality SEC Chair Gary Gensler has waged a frontal assault on crypto innovation. takes a dim view of innovation. He now seeks “plenary authority” over crypto including currency-like stablecoins.

Given the attested reserves and constant market adjustments, the chance Helen will lose her shirt or risk the financial system (absent fraud) is tiny. But government regulation carries much clearer risks. Regulators could easily become beholden to the biggest businesses they regulate. “Regulatory capture” would mean the biggest players join with regulators and lawmakers to write the rules and increase barriers to entry. This isn’t theoretical. Indeed, since the New Deal’s forlorn National Recovery Act, it has been a staple of U.S. economics.

And there is also the risk of stratification: Whatever rules regulators issue freeze current technologies at that time. This is particularly benighted given stablecoins’ role in fueling the unforeseen innovations of Web 3.0 where potentially billions of microtransactions occur every second. Helen may not only have her interest rate reduced, but the government could also deny her the benefit of the brightest minds currently conceiving ways to make her life richer and easier.

The Helens and Sams of this country ought to be able to choose the vehicles they wish for passive income and accept market risks that suit their appetite. Given the stablecoin market’s transparency, variety of choice, and constant adjustments, regulators have no problem to solve. Regulators themselves are the problem.

Americans are excited about crypto. Who can blame them? Digital currencies promise to eliminate the middleman in all value transfers, starting with financial markets. But no good deed goes unpunished, and federal regulators are growing panicked that their control might be diminished.

The recently passed infrastructure bill in Congress, President Biden’s Working Group report on stablecoins, the Securities and Exchange Commission’s “regulation by enforcement” policy, and the Federal Reserve’s flirtation with a Central Bank Digital Currency (CBDCs) all reveal Washington’s intent to scale back or even kill this blossoming industry.

Government crypto foes warn of systemic risks, insufficient consumer and investor protection, and inadequate reporting. Regulators can supposedly fix these maladies by forcing Americans to bypass wealth opportunities and surrender financial privacy. Instead of private digital currency, they’re eying central bank digital currencies, whereby a public ledger records and monitors all financial transactions. China is already implementing such a system. We’re assured a U.S. version would come with appropriate protections, but Tea Party activists and others who’ve had their taxes leaked over the past few years have cause to disagree.

Infrastructure Bill is a Crypto Nightmare

The recently passed Infrastructure Investment and Jobs Act (P.L. 117-58) is a step toward plenary crypto control. It would potentially force crypto miners and coders into service as government agents supplying Big Brother with transaction information they don’t currently have. The bill would bring new rules that could lump in as “brokers” too many professionals who provide crypto services but do not interact directly with cryptocurrency customers, as Competitive Enterprise Institute senior fellow John Berlau warned in a Forbes commentary.

Treasury Secretary Janet Yellen, chief proponent of the reporting requirements, exhibits scant understanding of how crypto works. Her priority is closing a $7 trillion “tax gap,” and she sees the mostly unorganized, anti-establishment crypto industry as easy pickings. Treasury officials defining and writing crypto rules under this provision could produce disastrous consequences, especially when China’s ban provides the United States a chance to become the world’s leader.

Congress needs to be more crypto friendly

Ideally, Congress’s job is to the check the ambitions of these runaway bureaucrats and constrain public power over the lives of citizens. One bill that would aid those causes is the bipartisan Keep Innovation in America Act, introduced by House Financial Services Committee Ranking Member Patrick McHenry (R-NC) and co-sponsored by House members of both parties. The bill would correct the worst crypto provisions of the infrastructure legislation.

Rep. McHenry and his colleagues should also prioritize reigning in Gary Gensler’s SEC. Despite Gensler’s crypto knowledge, he aligns with Yellen and the rest of the bureaucratic establishment. His singular focus on meting out regulatory punishments fails the moment. He has asked Congress for “plenary authority” over crypto and for budget increases so he can hire more regulators to bring endless lawsuits — supposedly to protect the little guy.

McHenry should also lead Congress in pulling regulators back from attacking Stablecoins pegged 1:1 to assets, mostly the U.S. dollar. The relatively tiny $145 billion market has proven resilient as its growth has exploded despite some well-publicized issuer accounting disputes. The Working Group wants to push these issuers into a suffocating federal framework that leaves little room for innovation.

Congress succeeded with the JOBS Act

Congress previously displayed admirable foresight. In 2012 it passed the bipartisan Jumpstart Our Business Startups (JOBS Act), signed into law by President Obama, which opened previously restricted investment opportunities in private markets. The equity crowdfunding provision of the JOBS Act, Title III (championed by McHenry), allowed ordinary people to invest in startups and local businesses. Back then, as today, bureaucratic worrywarts warned of impending doom. Then SEC chairwoman Mary Schapiro wrote the Senate Banking committee stating equity crowdfunding would subject Americans to “fraudulent schemes designed as investment opportunities.” Fellow commissioner Luis Aguilar insisted he could not “sit idly by when I see potential legislation that could harm investors. This bill seems to impose tremendous costs and potential harm on investors with little or no corresponding benefit.”

The SEC so opposed Title III it took four years to write the rules. The results are in: Equity crowdfunding has produced over $1 billion in investment to 4,5000 companies in 450 industries. It created tens of thousands of jobs the bureaucrats would have thwarted. Globally, the crowdfunding industry will double by 2027., the US would have lost a significant part of this growth.

In the same way equity crowdfunding decentralized startup capital and investing, resulting in a boon for startups and local economies start-up companies, crypto and its applications known loosely as Web3 will decentralize all information and value transfer. But this can’t happen if financial regulators dictate policies focused solely on risk. Congress must take a broader view and lead the way forward.

thecrowdfundinglawyers.com founder Paul H. Jossey will be a panelist at the popular annual DC Startup Week conference. Paul will discuss the legal aspects of equity crowdfunding on the panel Crowdfunding in 2021 and Beyond: What’s it Really Like.

Learn more about DC Startup Week and register for free here: https://www.eventbrite.com/e/dc-startup-week-2021-free-virtual-pass-limited-live-vip-conference-tickets-165149752355

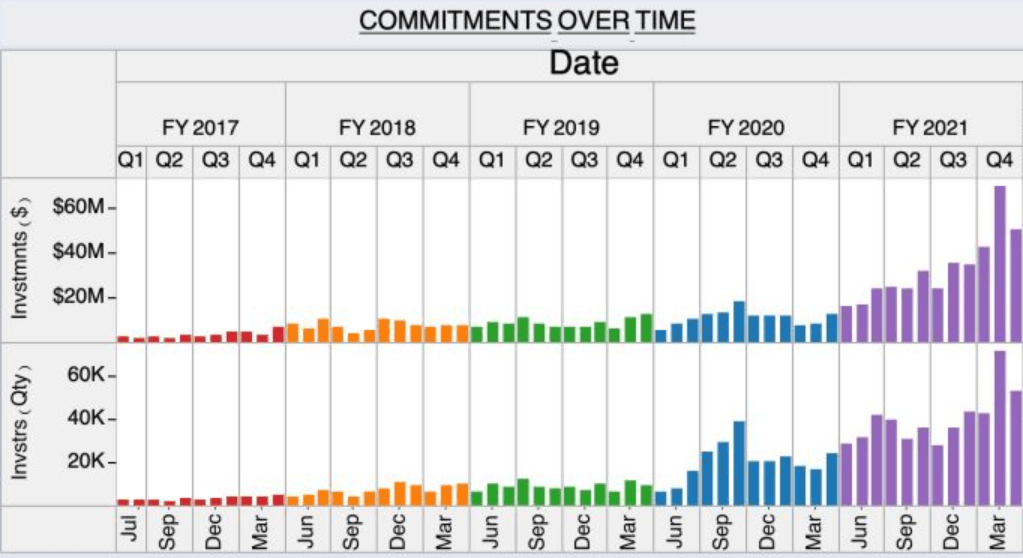

The numbers are in, and Regulation Crowdfunding (Reg CF) has had yet another blockbuster quarter, setting records across the board. According to Crowdfund Capital Advisors, which curates Reg CF data, year-over-year offerings are up 22%, investments up 93%, and investors up 22.3%.

The numbers continue Reg CF’s impressive climb up the private-investment chart. The exemption has now accounted for over one billion in commitments, by over one-million investors, through over four-thousand offerings. The average raise has climbed to $376, 939. The numbers remain tiny compared to behemoth Reg D, which accounts for over $1 trillion each year and outpaces the public markets. Yet Reg CF’s continued growth shows a fervent wish by startups to share their ideas and potential growth with retail investors and those investors’ desire to invest pre-IPO.

Source: Crowdfund Capital Advisors

The reasons for Reg CF’s explosive growth are varied

First is awareness. The exemption is the newest private-investment vehicle available in the US. Congress created it as part of the JOBS Act of 2012. The SEC did not finalize the regulations until 2016. After a slow start, the idea of ordinary people investing in early-stage companies has bloomed. This is true especially outside the traditional startup hotspots.

Second are SEC-implemented improvements. In a 2019 Concept Release, the SEC invited comment on ways to improve and streamline the various private exemptions, including JOBS Act provisions.

Public comment poured in, and the Commission listened. In November 2020 the Commission approved various changes to the private exemptions. For Reg CF this meant: (i.) greater issuer freedom to communicate with potential investors; (ii.) higher investor limits; (iii.) higher issuer offer limits; and (iv.) the availability of special purpose vehicles to place all Reg CF investors in one legal bucket and clean up cap table issues.

Third, the global pandemic forced companies and investors to rethink capital strategies. Limits on in-person meetings meant people looked online for investment. This fit perfectly with Reg CF’s investment-through-portal structure. As the CEO of SeedInvest, one of the biggest equity crowdfunding portals, explained earlier this year:

Unlike venture capital firms, online fundraising platforms are perfectly situated to help startups in the current, post-COVID-19 world we are in. Online fundraising platforms are not dependent on capital from a handful of pensions and endowments, but rather a large, diverse network of investors . . . Additionally, while the traditional venture capital investment process is highly dependent on in-person meetings (which is next to impossible in the current environment), the online fundraising and investing process is inherently digitally native.

Reg CF legal representation is more important than ever

Reg CF’s explosive growth will bring more SEC scrutiny, showing the need for legal representation. Although Reg CF has been essentially fraud free, the SEC brought its first enforcement action last month. This signals a growing interest by the Commission’s Enforcement Division in Reg CF offerings. Given this reality, it’s imperative Reg CF issuers have legal counsel guide them through the process. Those that do not are rolling the dice.

Reg CF will continue to change the startup-capital narrative. Although barely five years old, this exemption may prove the Reg D slayer as awareness grows, successes proliferate, and investor returns pour in.

“A digital economy is not simply an industrial economy on the internet.” The Blockchain Innovation Hub at the Royal Melbourne Institute of Technology in Australia recognizes a truth governments worldwide have not. Web 3.0, the approaching next internet phase with unprecedented methods of commerce, is unique in history. The Industrial Revolution transition is analogous. Changes of this magnitude require governments to reevaluate their economic oversight role. Web 3.0 will challenge old models of what constitutes a firm, a security, and a commercial transaction. The Royal Melbourne Institute provides some worthwhile proposals to welcome this new cyber world.

In the future, shareholders will run companies directly through smart contracts coded into decentralized applications—no management required. Cars will pay each other to pass or change lanes. Houses will rent out spare bedrooms upon predefined criteria. Computers will sell extra file storage to the continuously, to the highest bidder. And people will buy, share, and exchange value in myriad forms without any impeding central authority.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

A cookie is a string of information that a website stores on a visitor’s computer, and that the visitor’s browser provides to the website each time the visitor returns.

THECROWDFUNDINGLAWYERS.COM uses cookies to help identify and track visitors, their usage of THECROWDFUNDINGLAWYERS.COM sites, and their website access preferences. THECROWDFUNDINGLAWYERS.COM visitors who do not wish to have cookies placed on their computers should set their browsers to refuse cookies before using THECROWDFUNDINGLAWYERS.COM’s websites, with the drawback that certain features of THECROWDFUNDINGLAWYERS.COM’s websites may not function properly without the aid of cookies.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.